Contents

Brex is built for funded, global, travel-heavy companies. We ranked 8 alternatives on restaurant qualification, manager controls, receipt follow-up, and how cleanly each purchase reaches accounting.

Where Brex falls short according to users online

Brex is strong for funded, global, and travel-heavy teams. Public reviews plus Brex's pricing and support pages point to 6 tradeoffs restaurant operators should weigh.

- Qualification favors startup-shaped companies. Brex evaluates business model, funding source, and spend patterns. Its profiles lean toward equity-funded companies, $1M+ revenue, or referred tech startups, and startup monthly billing carries a $50,000 cash-balance minimum. Source: Brex account requirements page, June 2026

- The 2022 small-business exit still shapes buyer trust. Brex told many smaller customers it would close their accounts by August 15, 2022. It kept companies with venture backing, $1M+ revenue, 50+ employees, or $500K+ in cash. Sources: TechCrunch, June 2022; Brex's June 2022 announcement

- The features growing groups need can move into paid seats. Multi-entity support, live budgets, budget delegation, HRIS integrations, and custom accounting integrations live in Premium at $12/user/month. For a 4-entity restaurant group, table-stakes controls become per-user math. Source: Brex pricing page, June 2026

- Credit-limit and account-hold complaints recur in reviews. Trustpilot reviewers describe credit lines cut sharply or accounts paused during compliance reviews. Those are anecdotes, not the average experience, but weekly restaurant cash flow has less room for surprise holds. Source: Trustpilot reviews, June 2026

- Rewards are points, not cash. Brex publishes no flat cash-back rate; value depends on how you redeem, and travel-weighted redemptions assume a team that travels. On restaurant margins, a predictable cash rebate usually beats a points balance someone has to manage. Source: Brex pricing and rewards pages, June 2026

- Capital One ownership adds a roadmap question. Capital One's $5.15B Brex deal gives the product big-bank backing. It can also change pricing, underwriting, or roadmap priorities, so verify current terms before a long commitment. Sources: Capital One announcement, April 2026; Financier Worldwide

None of this makes Brex a bad platform. It makes Brex a specific platform, and the rest of this article is about what to use when your business is not the one it was built for.

How we chose the best Brex alternatives

A replacement only counts as an upgrade if it fixes the reason you are leaving. Most lists of Brex competitors chase the same startup buyer Brex does, so we scored each alternative on the work a restaurant needs the card program to do instead:

- Restaurant fit. Does the product understand locations, vendors, operators, and shift-level purchases, or does it assume generic corporate employees?

- Qualification. Can a bootstrapped operator actually get approved without venture backing or a credit check?

- Pricing and fees. What does the program cost at 10, 30, or 80 cardholders, including per-user seats, platform fees, and payment fees?

- Card controls managers actually use. Custom limits, instant issuing, and assignment by employee and location, enforced at the swipe rather than reported after it.

- Receipt and accounting automation. Does the platform chase receipts and sync coded transactions to QuickBooks, or does your bookkeeper inherit the cleanup? Restaurant expense automation is built to reduce that follow-up.

- Entity and bank-account fit. Can the platform map spend to locations, LLCs, bank accounts, and QuickBooks or Restaurant365 exports without manual sweeps?

We also weighed replacement risk: how disruptive each option is to adopt, and what you give up by leaving Brex's all-in-one stack. If the category is new to you, this primer on modern corporate and purchasing cards for restaurants explains why restaurant card programs became their own product category.

Brex fit check for restaurants

This table shows where Brex tends to fit and where restaurant-specific workflows may matter more.

| Question | Brex is likely strong if... | Look beyond Brex if... |

|---|---|---|

| What kind of company are you? | Large enterprise, funded tech company, or hospitality group with global travel | Independent restaurant or multi-location group that needs hospitality workflows |

| What is the card's biggest job? | Travel, software, global card controls, treasury | Managers, locations, receipts, vendor purchases, QuickBooks close |

| What support model do you need? | Standard fintech support is fine | Restaurant-aware onboarding and support matter |

| What caused this search? | You need more global finance features | Eligibility, credit or limit changes, small-business fit, or restaurant workflow gaps |

| What data must close cleanly? | ERP and global entity data | Location, LLC, bank account, GL code, receipts, QuickBooks or Restaurant365 |

The right column is the restaurant lane. Brex facts verified June 2026 on Brex's published materials.

A restaurant group can land in both columns. If that is you, the honest play is a restaurant-native card program for operations spend, with Brex kept only if a corporate team genuinely needs its enterprise travel or global stack.

Brex alternatives at a glance

| # | Alternative | Best for | Pricing | Rewards / terms | Key caveat |

|---|---|---|---|---|---|

| 01 | Restaurant groups that need cards, receipts, locations, LLCs, bank accounts, and accounting exports handled | Base is free; Pro $150/month/location | unlimited cash back on Base; Pro adds Andy AI and dedicated support | Built for restaurant financial flows | |

| 02 | ERP-heavy finance teams with broad corporate spend | Free; Plus $15/user/month + platform fee | Cash back on card spend | Bill-pay fees from June 2026; priced per user | |

| 03 | Owners who want $0 fees and flat cash back | No platform, subscription, or per-card fees | Up to 1.5% cash back | Daily auto-debit repayment by default | |

| 04 | Teams that overspend and want budgets enforced up front | Free software with the BILL Divvy Card | Rewards scale with payoff frequency | Credit lines determined at application, not guaranteed | |

| 05 | Operators who want excellent banking first, card second | Free banking; paid plans from $29.90/month | IO card 1.5% unlimited cash back | Light expense and reimbursement tooling | |

| 06 | Teams whose card spend is mostly travel | Expense free for first 5 users, then $15/user/month | Travel and expense in one platform | Travel-first product; restaurant ops absent | |

| 07 | Fixing expense reports on cards you already have | Collect $5/member/month; Control from $9/member/month | Up to 2% cash back with the Expensify Card | Per-member fees stack; support complaints in reviews | |

| 08 | Groups with real cross-border operations | Explore $0/user/month; Grow $12/user/month + platform fee | Up to 1.5% rebates on local USD spend; 0.5% to 1% FX | Global tool; account-freeze complaints in reviews |

Pricing and rewards verified June 2026 on each provider's published pricing. Terms change; confirm before applying.

The 8 best Brex alternatives, ranked

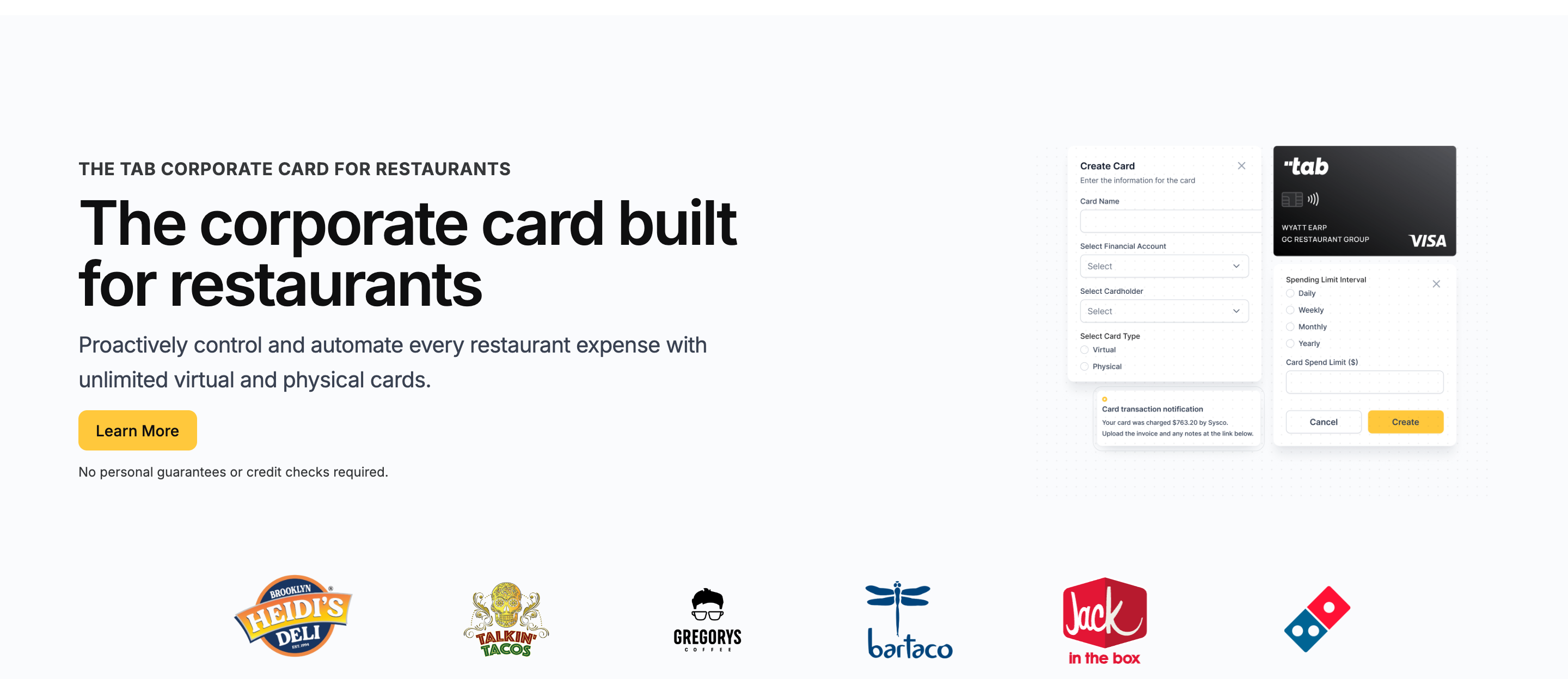

Tab

Best for restaurantsBest Brex alternative for restaurants, from a single unit to a multi-location group.

Tab answers the qualification question before anyone asks it. It is a finance platform built for restaurant financial flows, used by 1,000+ restaurants, and its card requires no credit check. Nobody asks who funded you.

- Underwriting fits restaurants, not funding rounds. Where Brex underwrites your funding profile, Tab underwrites the way restaurants actually operate, with no credit check.

- Cards scoped to the job. Issue unlimited virtual and physical Visa cards, set custom limits, and assign each card to an employee, one or more locations, and even specific vendors.

- Receipts stop being archaeology. After every swipe, the cardholder gets a text and email prompt to snap the receipt, add a note, and tag the location, with multi-location splits for orders that cover 2 stores.

- Multi-entity workflows are native. For groups with multiple LLCs and bank accounts, Tab supports multi-LLC and multi-bank workflows that map spend and repayment to the right location or entity.

- The books arrive clean. Transactions sync through a full QuickBooks Online integration, and Restaurant365 users can work with Tab on custom export files.

- Andy adds expense intelligence. On Pro, Andy AI digitizes distributor invoices, checks line-item prices, and surfaces rebate or contract issues.

Cash flow flexes by how you pay. Base includes unlimited cash back, receipt capture, location tagging, and a full QuickBooks Online integration. Account-specific repayment details should be verified with Tab. All of it is cash, not points, which matters when margins live in single digits.

Tab reports a 90-second average text receipt submission time and 85%+ higher accounting accuracy, with support from real humans based in the US and Canada.

Operators evaluating the field have made the comparison already. Rock Strategic runs 75+ units on Tab, and the quote above comes from Tab's card launch announcement. Heidi's Brooklyn Deli runs 8+ locations on the platform.

- Best forRestaurant operators, single unit to multi-location group

- PricingBase free; Pro $150/mo/location

- Rewardsunlimited cash back on Base

- Built forRestaurant financial flows

What you get on the free plan:

- Unlimited virtual and physical cards

- Custom limits by employee, location, and vendor

- Automated receipt capture by text and email

- Full QuickBooks Online integration included

- Unlimited cash back, no annual fee

- Live US-based human support

Pricing: Tab's Base plan is free and includes Tab Cards, Accounts, unlimited cash back, receipt capture, the full QuickBooks Online integration, and live US-based support. Pro is $150/month/location and adds Andy AI for distributor invoice intelligence, price checks, rebates, and contract visibility, plus a dedicated Account Manager. Groups with 5+ locations get custom pricing.

Best for: Restaurant operators who want one card program for limits, receipt follow-up, restaurant and entity details, and accounting exports. Brex may fit large enterprise, global, or travel-heavy teams better; the full Tab vs Brex comparison walks that decision line by line.

Ramp

Best generic Brex alternative for ERP-heavy finance teams with broad corporate spend.

Ramp is a broad corporate spend platform: cards, expense management, bill pay, procurement, and travel in one system. It fits teams with dedicated finance owners and ERP-heavy workflows better than local restaurant operators.

Against Brex

Ramp pays rewards as cash back on card spend rather than points, and QuickBooks Online and Xero integrations sit on its free tier. Both platforms start at $0, so the real comparison is which paid tier your team grows into and which rewards model you prefer.

- Best forERP-heavy finance teams

- PricingFree; Plus $15/user/mo + platform fee

- RewardsCash back on card spend

- What to weighBill-pay fees from June 2026

Where it wins

- Deep policy controls. Employee cards with enforced limits, approval workflows, and accounting automation for office finance teams.

- Deep accounting integrations. QuickBooks Online and Xero on the free tier; NetSuite and Sage Intacct on the paid plan.

- A genuinely free base tier. Cards and core spend management at $0 to start.

Where it falls short

- Nothing restaurant-native. No location tagging, vendor-assigned card logic, or POS-aware cash view; Ramp is built for broad finance teams.

- Per-user pricing compounds. Plus runs $15/user/month billed annually plus a platform fee, painful when restaurants hand cards to a lot of users.

- Bill pay stops being free. From June 1, 2026, standard ACH costs $0.59 and checks $1.99 unless paid from a Ramp account.

Pricing: Free base tier; Plus is $15/user/month billed annually plus a platform fee based on team size (verified on Ramp's published pricing overview, June 2026).

Ramp

Brex

Tab (reference)

Pricing verified June 2026 on each provider's published pricing.

What to weigh

- Per-user pricing compounds in restaurants. Plus runs $15/user/month billed annually plus a platform fee based on team size, and restaurants hand cards to a lot of users.

- Bill pay stops being free. Effective June 1, 2026, standard ACH payments cost $0.59, same-day ACH $10, domestic wires $15, and checks $1.99 unless paid from a Ramp account.

- No restaurant workflows. There is no location tagging, vendor-assigned card logic, or POS-aware cash view. If ordering and receiving are the actual pain, compare the tools in this restaurant procurement software guide.

Best for: Restaurant groups with a real finance team, stronger cash balances, and mostly general corporate spend. If Ramp is your front-runner, the deeper look at Ramp alternatives for restaurants covers where it fits and where it strains.

Rho

Best $0-fee banking and card alternative with flat cash back.

Rho strips the fee structure down to nothing: no platform fees, no subscription fees, no per-card fees, and up to 1.5% cash back on card spend. It pairs corporate cards with business banking in one account.

Against Brex

Rho's pitch is simplicity where Brex's is scale. You get a flat cash rebate instead of a points program, and Rho says its card does not require a personal credit pull, so qualification does not hinge on a funding story. The card runs on Mastercard, issued via Webster Bank.

- Best for$0-fee flat cash back

- PricingNo platform, subscription, or card fees

- RewardsUp to 1.5% on card spend

- What to weighDaily auto-debit by default

Where it wins

- The most honest fee structure here. No platform, subscription, or per-card fees, with real-time controls and accounting sync included.

- Up to 1.5% flat cash back on card spend, no category tiers to game.

- No personal credit pull currently required to qualify.

Where it falls short

- You bank where you card. Repayment auto-debits daily from your Rho checking account unless you apply for monthly terms.

- A 3% late fee applies to delinquent balances, which stings during a slow month.

- No restaurant-aware features. Location tagging, vendor card assignment, and receipt chasing for hourly teams are not part of the product.

Pricing: No platform, subscription, or per-card fees (verified on Rho's corporate cards page, June 2026).

Rho

Brex

Tab (reference)

Pricing verified June 2026 on each provider's published pricing.

What to weigh

- Repayment is a daily auto-debit by default. Rho pulls payment from your Rho checking account daily unless you apply for monthly terms, so your operating cash effectively needs to live at Rho.

- Late balances carry a 3% fee. Delinquent amounts are charged 3%, which stings during a slow month.

- No restaurant-aware features. Location tagging, vendor card assignment, and receipt chasing built for hourly teams are not part of the product.

Best for: Lean operations that want modern cards and banking with zero software cost, and are comfortable moving their primary operating account to Rho.

BILL Spend & Expense (formerly Divvy)

Best budget-first alternative for boxing in spend before it happens.

BILL Spend & Expense comes at spending from the opposite direction: set the budget first, then let cards enforce it. You build a budget for repairs or smallwares, assign people to it, and cards simply decline past the cap.

Against Brex

Qualification is not tied to venture funding. BILL advertises credit lines from $1K to $5M with the free software included alongside the BILL Divvy Card, though it is explicit that lines are determined at application and not guaranteed. For a team that overspends, pre-set budgets are a stronger control than any after-the-fact policy engine.

- Best forBudget-first spending discipline

- PricingFree software with the Divvy Card

- RewardsScale with payoff frequency

- What to weighCredit lines not guaranteed

Where it wins

- Budgets enforce themselves. Genuinely effective discipline for teams whose problem is overspending, not reconciliation.

- Free software with the card. No annual fee alongside the BILL Divvy Card.

- Credit lines from $1K to $5M advertised, sized at application.

Where it falls short

- Rewards take explaining. Rewards scale with how often you pay your balance off, so two operators on the same card can earn differently.

- Credit lines can move. G2 reviewers report limit cuts and account freezes with little warning.

- Accounting sync needs babysitting. Reviewers describe QuickBooks syncs requiring extra manual steps and support slowing down after onboarding.

Pricing: Free software with the BILL Divvy Card; no annual fee; credit lines $1K to $5M, not guaranteed (verified on BILL's product pages, June 2026).

BILL Spend & Expense

Brex

Tab (reference)

Pricing verified June 2026 on each provider's published pricing.

What to weigh

- Rewards take explaining. Rewards scale with how often you pay your balance off, so two operators on the same card can earn differently.

- Credit lines can move. G2 reviewers report limit cuts and account freezes with little warning, echoing the credit-line complaints in BILL's G2 reviews.

- Accounting sync needs babysitting. Reviewers describe QuickBooks syncs requiring extra manual steps and support slowing down after onboarding.

Best for: Single-location or small-group operators whose core problem is overspending, not reconciliation, and who want budget discipline enforced at the card.

Mercury

Best banking-first alternative with a simple flat cash-back card.

Mercury starts with the bank account, not the card. Free checking and savings with $0 maintenance fees and $0 USD wires, a clean interface, and the IO credit card attached: 1.5% unlimited cash back, no annual fee, and no credit check.

Against Brex

If the thing pushing you off Brex is banking, Mercury is the cleaner bank. Wires are free, the free tier is genuinely free, and Treasury offers up to 3.60% yield on balances over $250K. The trade is that cards and expense tooling are the side dish rather than the meal.

- Best forBanking first, card second

- PricingFree banking; Plus $29.90/mo; Pro $299/mo

- RewardsIO card 1.5% unlimited cash back

- What to weigh5-user reimbursement cap on free tier

Where it wins

- Genuinely free banking. $0 maintenance fees and $0 USD wires on a clean, modern interface.

- Simple flat cash back. The IO card earns 1.5% unlimited cash back with no annual fee.

- No credit checks to qualify for the card.

Where it falls short

- Expense features are capped on the free tier. Reimbursements cover only 5 users per month until you pay for Plus at $29.90/month.

- Deep accounting automation costs $299/month. NetSuite-grade automations require the Pro tier.

- No receipt chasing for hourly teams. There is no location tagging or restaurant context anywhere in the product.

Pricing: Free banking; Plus $29.90/month; Pro $299/month for NetSuite-grade automation (verified on Mercury's pricing page, June 2026).

Mercury

Brex

Tab (reference)

Pricing verified June 2026 on each provider's published pricing.

What to weigh

- Expense features are capped on the free tier. Reimbursements cover only 5 users per month until you pay for Plus at $29.90/month.

- Deep accounting automation costs $299/month. NetSuite-grade automations require the Pro tier.

- No receipt chasing for hourly teams. There is no location tagging or restaurant context anywhere in the product.

Best for: Owners whose actual complaint is their bank, who want flat cash back on a simple card and can live with thin expense tooling.

Navan

Best travel and expense alternative when trips are the real spend.

Navan is what you pick when the spend you care about happens on the road. It combines corporate travel booking with expense management, free for companies up to 300 employees on the travel side, with expense management free for the first 5 users and $15/user/month after that.

Against Brex

Brex includes travel booking, but Navan is travel-native: inventory, policy workflows, self-serve changes, and 24/7 trip support are the core product rather than a module. If a franchise development team or multi-market leadership group lives in airports, that depth shows.

- Best forTravel-heavy leadership and dev teams

- PricingExpense free for 5 users; $15/user/mo after

- RewardsTraveler rewards on bookings

- What to weigh$15/user after 5 expensing users

Where it wins

- Travel-native depth. Inventory, policy workflows, self-serve changes, and 24/7 trip support are the core product.

- Travel free up to 300 employees. A genuine free tier for the booking side.

- Travel and expense in one. Bookings and expensing live under a single platform.

Where it falls short

- Expense pricing kicks in fast. Free covers only the first 5 monthly expensing users; a 30-manager group pays $15/user/month for the rest.

- Support strains during disruptions. Reviewers praise day-to-day ease but flag slower support during peak travel disruptions and recurring mobile app bugs.

- Restaurant operations are absent. No location-level spend logic, no vendor card workflows, no receipt capture designed for restaurant operations.

Pricing: Travel free up to 300 employees; expense free for the first 5 users, then $15/user/month (verified on Navan's pricing page, June 2026).

Navan

Brex

Tab (reference)

Pricing verified June 2026 on each provider's published pricing.

What to weigh

- Expense pricing kicks in fast. Free covers only the first 5 monthly expensing users; a 30-manager restaurant group would pay $15/user/month for the rest.

- Support strains during disruptions. G2 reviewers praise day-to-day ease but flag slower support during peak travel disruptions and recurring mobile app bugs.

- Restaurant operations are absent. No location-level spend logic, no vendor card workflows, no receipt capture designed for restaurant operations. If formal travel and expense is the job, compare the wider field in this Concur alternatives guide.

Best for: Restaurant groups with a genuine travel program: franchise development, multi-market executives, conference-heavy leadership. For daily vendor spend, look elsewhere on this list.

Expensify

Best expense-reporting alternative on top of the cards you already have.

Expensify is the one option here that does not ask you to switch cards at all. It is expense software first: SmartScan receipt capture, approval flows, and accounting sync layered over whatever bank and cards you already run, with an optional Expensify Card.

Against Brex

Brex wants to become your finance stack; Expensify just wants your receipts. If your bank relationship and cards are fine and the pain is purely expense reports, a $5/member/month Collect plan is a much smaller move than re-platforming.

- Best forReports on cards you already run

- PricingCollect $5/member/mo; Control from $9

- RewardsUp to 2% with the Expensify Card

- What to weigh$9 tier needs annual + card spend

Where it wins

- No re-platforming required. SmartScan receipt capture and approval flows layer over the bank and cards you already run.

- A small starting move. Collect runs $5/member/month, month-to-month, far cheaper than switching stacks.

- Up to 2% cash back with the optional Expensify Card on Control.

Where it falls short

- Per-member fees stack with caveats. Control is $9/member/month only with annual billing and 50%+ US spend on the card; it is $18 without the card and $36 pay-per-use.

- Billing and support complaints recur. Reviewers cite surprise billing practices and slow, automated support responses.

- It is a reporting layer, not a card program. Spend controls, underwriting, and banking remain your job; restaurants still stitch locations and vendors together manually.

Pricing: Collect $5/member/month; Control $9, $18, or $36/member/month depending on setup (verified on Expensify's billing documentation, June 2026).

Expensify

Brex

Tab (reference)

Pricing verified June 2026 on each provider's published pricing.

What to weigh

- Per-member fees stack with caveats. Control costs $9/member/month only with an annual subscription and 50%+ of US spend on the Expensify Card; it is $18 without the card and $36 pay-per-use.

- Billing and support complaints recur. Reviewers on Capterra, where Expensify holds a 4.4-star average across 1,100+ reviews, cite surprise billing practices and slow, automated support responses.

- It is a reporting layer, not a card program. Spend controls, underwriting, and banking remain your job; restaurants still stitch locations and vendors together manually.

Best for: Teams keeping their existing bank and cards who only need receipts, reports, and reimbursements handled.

Airwallex

Best global account and card alternative for cross-border operations.

Airwallex exists for money that crosses borders: multi-currency business accounts, local transfers to 120+ countries, and corporate cards with up to 1.5% cash rebates on local USD spend. The Explore tier starts at $0/user/month.

Against Brex

This is the FX matchup. Airwallex converts currency at 0.5% above interbank rates for major currencies and 1% for others, while Brex applies an FX markup of up to 3% on card transactions that need conversion. A hospitality group importing wine, equipment, or ingredients feels that spread.

- Best forReal cross-border operations

- PricingExplore $0; Grow $12/user/mo + platform fee

- RewardsUp to 1.5% rebates on local USD spend

- What to weighAccount-freeze complaints on Trustpilot

Where it wins

- Genuine cross-border reach. Multi-currency accounts and local transfers to 120+ countries.

- Low FX spread. Currency converts at 0.5% above interbank for major currencies and 1% for others.

- A free starting tier. Explore runs $0/user/month with up to 1.5% cash rebates on local USD spend.

Where it falls short

- Account freezes dominate complaint threads. Frozen funds and slow verification are the most common recent complaints.

- Paid features are per-user plus a platform fee. Grow runs $12/user/month plus a platform fee based on team size.

- It is not a US restaurant tool. Spend management exists, but nothing in the product addresses locations, vendors, or restaurant accounting workflows.

Pricing: Explore $0/user/month; Grow $12/user/month plus a platform fee; FX at 0.5% to 1% above interbank (verified on Airwallex's US pricing page, June 2026).

Airwallex

Brex

Tab (reference)

Pricing verified June 2026 on each provider's published pricing.

What to weigh

- Account freezes dominate complaint threads. Airwallex holds a 3.4-star average on Trustpilot, where frozen funds and slow verification are the most common recent complaints.

- Paid features are per-user plus a platform fee. Grow runs $12/user/month plus a platform fee based on team size.

- It is not a US restaurant tool. Spend management exists, but nothing in the product addresses locations, vendors, or restaurant accounting workflows.

Best for: Restaurant or hospitality groups with international supply chains, entities, or currency needs. Groups that buy and pay only in US dollars may not need the cross-border depth.

The verdict: which Brex alternative should restaurants choose?

Match the alternative to the reason you are leaving:

Decision rules

- Your managers spend daily across one or more locations: Tab is worth considering for card limits, receipt texts, location and LLC details, a full QuickBooks Online integration, and customizable exports.

- You want broad corporate spend automation: Ramp may fit, with Plus seats and its platform fee included in the cost model.

- You want zero fees and flat cash back: Rho may fit if the restaurant will bank there, while Mercury puts banking quality first.

- Overspending is the problem: BILL Spend & Expense centers the decision on card budgets.

- Your cards are fine and reports are the pain: Expensify focuses on reports and reimbursements.

- Travel or cross-border payments dominate: Navan focuses on trips, while Airwallex focuses on currencies.

- You are a large enterprise, global, or travel-heavy hospitality group that clears Brex's requirements: staying put is a defensible call.

For most restaurant operators, the decision comes down to what happens after a manager buys something. Tab is designed to collect the receipt, attach the restaurant and entity, and prepare the transaction for the accounting workflow, while the other options lead with broader corporate, banking, travel, or international jobs.

If you are still weighing card programs more broadly, the guide to the best credit cards for restaurant owners ranks issuer rewards cards alongside corporate card platforms.

FAQ

Tab is a direct Brex alternative to consider when restaurants need manager cards with limits, receipt prompts by text, location and LLC details, a full QuickBooks Online integration, and customizable exports. Brex may fit large enterprise, global, and travel-heavy teams better.

Brex can serve a large restaurant or hospitality group with corporate travel, global entities, and a finance team to run it. A local operator may not need that scope, especially when rewards accrue as points and restaurant workflows such as location tagging, vendor-assigned cards, and Restaurant365 exports are not native.

It depends on the small business. Brex's account requirements page describes profiles built around equity funding, more than $1 million in annual revenue, or referred tech startups, so a bootstrapped business under those thresholds sits outside its published profiles. Small businesses outside that lane usually fit better with Tab (restaurants), BILL Spend & Expense, or Expensify.

In June 2022, Brex told tens of thousands of smaller customers it would close their accounts by August 15, 2022, and clarified it would keep companies with equity investment, more than $1 million in revenue, more than 50 employees, or more than $500K in cash. It was a one-time, dated decision rather than a published current policy, and Brex has since been acquired by Capital One in a deal completed April 7, 2026.

Brex Essentials is already $0/user/month, so the costs that matter are Premium seats at $12/user/month, FX markup up to 3%, and points instead of cash back. Tab's Base plan, Ramp's free tier, BILL Spend & Expense with the Divvy Card, Rho, and Mercury banking are all free to start. For restaurants, Tab keeps controls, receipts, and the QuickBooks feed on its free plan.

Count the people holding cards, the restaurants they buy for, and the accounting work after each purchase. Ramp may fit broad corporate spend and ERP-heavy automation. Brex may fit large global or travel-heavy groups. Tab focuses on restaurant-level limits, receipt texts, location and entity details, a full QuickBooks Online integration, and customizable exports.

The bottom line

Brex did not fail restaurants; it was built for a different company profile. Its underwriting, rewards, and roadmap may suit large global teams, while the 8 alternatives here give restaurant operators other ways to handle location-level spend.

If managers spend, receipts go missing, and QuickBooks Online is where it all has to land, see how Tab's restaurant card handles limits, receipts, and location tagging. The Base plan is free, and setup takes about one week and is ready for the first billing cycle.

James writes from Tab's work with restaurant groups choosing cards, receipt workflows, accounting handoffs, and support. Tab builds the AI-powered finance platform for restaurants: cards, accounts, payments, automation, and intelligence in one back office.